So I started off my twenties with a few key money moments:

- I graduated college with $25,000 of student loan debt.

- I promptly got my credit card declined at a bar trying to buy a $5 rum and coke.

I’m almost 30 and managed to turn my financial life around somewhat.

I’m now paying for an expensive apartment in Seattle and still eating breakfast for dinner once per month.

I did pay off $100,000 of debt, get married for under $15,000 and save $26,000 in 7 months.

Things are looking up, right?

Here are the 10 money goals I want to cross off my list before 30.

Do you agree or disagree?

PS – if you want to learn more about my money journey and this site, Millennial Boss, go here.

1. Stop living 1-2 paychecks in the future

This sounds simple but so many people are living 1-2 paychecks in the future.

Meaning, they spend on their credit cards and need to wait until their next paycheck hits to pay them off.

If this is you, cut back for 30 days, build up your cash reserve and stop the constant catch up.

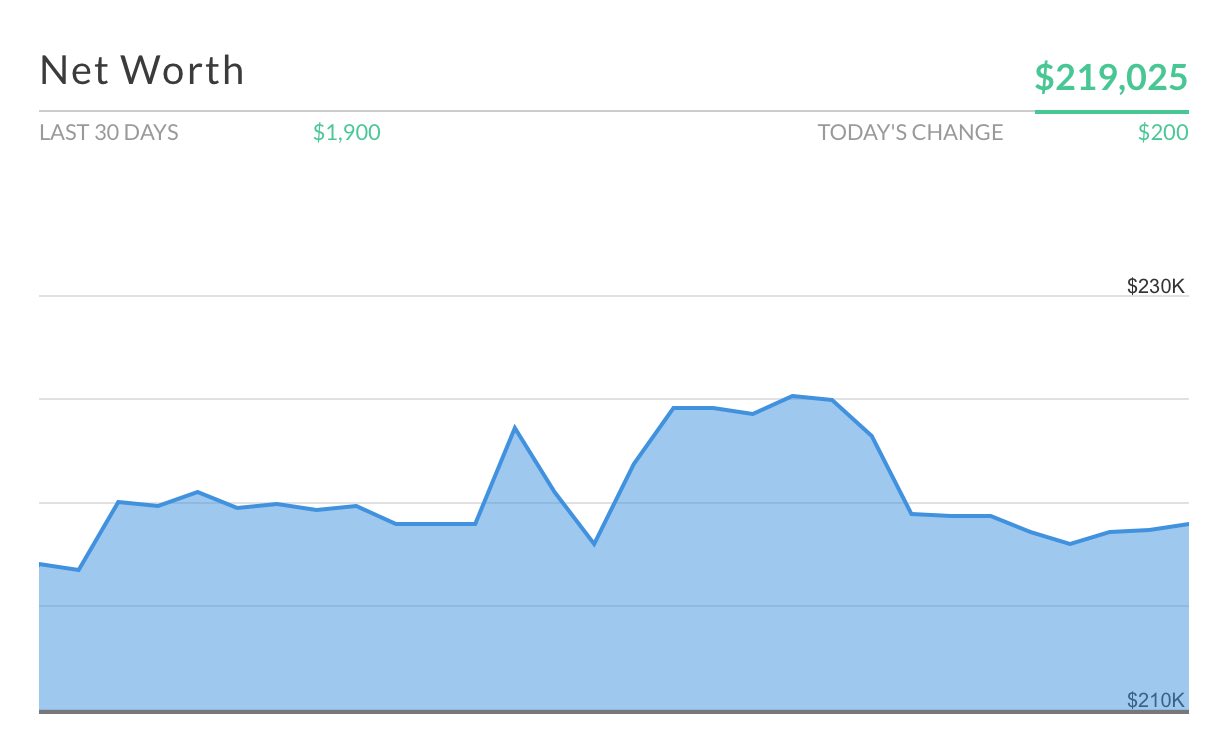

2. Know your net worth

Do you know your net worth?

Use a free mobile app, such as Personal Capital, to track your expenses and calculate your net worth total.

From age 26 to 28, I increased my net worth to over $200,000 after I started tracking it with this app.

Sign up here for Personal Capital (it’s free).

By 30, you’ll definitely want to know your net worth number.

3. Pay off your student loans (or refinance)

You can lower your monthly payment and pay less interest in the long term by refinancing your loans with a new company.

You’ll hopefully pay off the loans faster and free up that money for investing and saving.

Federal interest rates were 6.8% when I was in college and I wish I had refinanced my student loans instead of paying that crazy interest rate for years.

Check out SoFi to refinance the student loans into a lower interest rate.

Take this quick survey to see if you qualify for a better interest rate: SoFi Survey

Related: How I Paid off $89,000 of Student Loan Debt in 18 Months

4. Max out your work retirement plan – 401(k), 403(b), etc.

This is a stretch goal for many but a good goal for a twenty-something (or anyone) to work towards.

Boost your annual retirement plan contribution by putting in the maximum you can contribute per year ($18k).

These contributions lower your taxable income (meaning you pay less in taxes now) and can grow significantly over time.

If you don’t have a work retirement plan consider opening an IRA with Vanguard or a similar company.

5. Have a side hustle!

I’m all about side hustles and love to get the most money for the least effort (plus it’s nice to have extra money coming in on top of your day job).

Below are the ways you can side hustle in the next 15 minutes.

Airbnb – rent out your home or a room in your home

Turo – rent out your car to people on vacation or on work trips

DoorDash – deliver food to people

Swagbucks – take online surveys for gift cards or cash

Looking for a more creative side hustle? Consider starting a blog.

I made $25k last year blogging. Here’s how.

6. Have $10k in a savings account for emergencies

We’ve all done the savings to checking account dance at some point in our lives – you know, when you realize you don’t have enough in your checking account so you have to pull from your savings.

Hopefully that no longer happens at 30 and the money in your savings can stay there for emergencies.

Related Post:

7. Get rid of your car payment

You can get rid of your car payment by selling your car (like I did last year), or you can just pay it off aggressively.

It stinks to have a car payment past 30.

Related: What it was like to live without a car the past year

8. Know your Credit Score

Your credit score is used to get the best interest rates on home mortgage purchases, car loans, etc.

A bad credit score could cost you thousands in the long run.

Many people have no idea what their credit score is.

I use Credit Sesame which tracks my credit score for free and notifies me of anything suspicious going on with my credit.

I love the app and it’s really easy to use.

Check your credit score here (with no impact to your score) with Credit Sesame for free.

9. Know how home buying works

Buying a home is not for everyone, but by thirty – most people should know how it works, but so many don’t.

Look into how mortgages work, understand the current interest rates, determine how taxes, insurance, and other expenses fit into a budget, and last know how different down payment amounts affect the mortgage payment.

Don’t get yourself saddled into debt while buying your first home because you don’t know how it all works.

(And know how home selling works too. We just sold our home for $100k more because we made these 10 home upgrades).

10. Start investing on your own too

We mentioned work retirement plans and individual retirement plans but what about individual investing accounts?

By 30, an individual should know how to invest on their own.

These individual investing accounts are also known as brokerage/taxable accounts and they’re a ticket to getting ahead financially.

You can open one up in two minutes and $5 with Betterment and start investing ASAP.

Betterment has robo-advisors so you don’t have to pay someone to choose your investment strategy. It does it for you.

Open a free account here with Betterment.

BONUS ** Have a financial plan for 40

Roadmap out the next decade financially and become a master of your money by 40.

My personal quest is to reach financial independence and have the possibility to retire early.

I want to retire before age 40.

Never heard of retirement that early?

Read more about the movement of young people who want to retire early here:

The Secret Cult of Young People Who Retire Early.

How are the top 1% doing at 30?

According to these sources:

- The top 1% of earners at age 30 make $173,000 per year .

- The top 1% of savers by age 30 have just under $200,000 saved.

Are you close or far away?

What are the top money goals for age 30 in your opinion?

Related Posts:

- Blogging Made Me $25,000 Last Year – Here’s My 7 Day Challenge for You

- Hacking My Engagement Ring for $300

- How to Make a Backyard Movie Theater with a projector screen - September 19, 2020

- HONEST Passive Income Planner Girl by Michelle Rohr course review - May 25, 2020

- 35 Pink Aesthetic Wallpapers with Quotes and Collages - May 20, 2020

Timely, as I turn 30 in two months from tomorrow! I’m reasonably happy with where we are at financially and I have a fuzzy goal of reaching FI by 45, but I need to buckle down and really lay out what it will take to get there.

Great list Millenial Boss! I need to get my taxable brokerage account going. I’ve maxed 401k and our Roth IRAs and am now working on the HSA by January. After that and paying off of our mortgage in December, it is time to focus on real estate investing and a taxable brokerage account. Hope to meet you at FinCon!

These are great tips! Luckily, my debt is paid off and my cost of living is SUPER low (I live on a sailboat), so now my goal is to make enough to travel by boat and put some into savings/investments for the future. Living below your means is key!

I’m (hopefully) going to graduate in May and then I plan on being pretty aggressive with my student loans. I can’t wait to be debt-free!

All great points, and I think especially #10. Having a goal 5 or 10 years out is such a motivator to do the everyday things that’ll get you there.

Great post! I still have 2 more years to build that 1 year emergency fund.

Suddenly feeling the pressure! 😉

Great list! I especially like number 10, I’ve always been a scared to calculate that one!

I’m 27 and my goal before I’m 30 is to have paid off the mortgage on my apartment. Next up is a speedy pay-off of my student loan..

I was kind of down when I turned thirty – but I have a goal of $1m net worth with no debt by the time I’m forty (about seven years). I just started tracking my net worth in the beginning with this year, and it’s nice not only to see the progress I’ve made, but the my goal will be easily obtainable!

Even though I am at above 40 I just paid of my credit card loan yesterday. I am debt free now and eager to save more money. Thanks to this post.